Mid-Year Update

“Be like a duck. Calm on the surface, but always paddling like the dickens underneath.” - Michael Caine

I hope everyone had a happy and safe 4th of July weekend. The story of Rip Van Winkle is always one I like to think about in the context of an investors’ portfolio over the long term, as it’s a story of a man that falls asleep and wakes up twenty years later, missing the American Revolution. The other anecdote, or quote, I like is the above, or some variation of it, as it really makes me think about all the things going on beneath the surface and how looks can be deceiving.

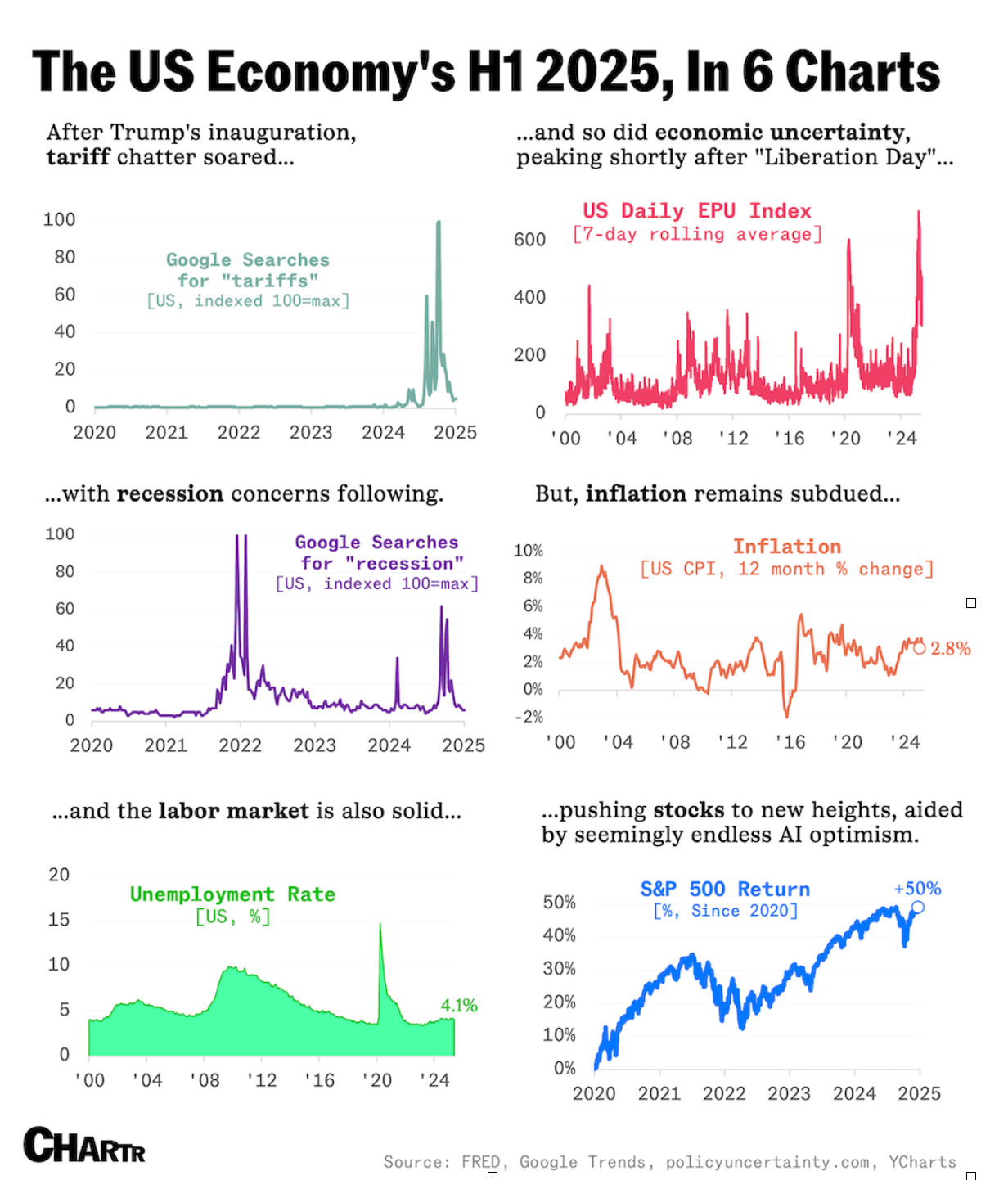

CHARTR is one of my favorite resources for charts and tidbits of information. I think they did a good job summarizing some of the key points in the first half of this year…

It has been a little while since we have last written, so we will start with some things we have been following closely, but have NOT really had an impact directly on the overall market as of yet…

Geopolitical Events

Ukraine/Russia. This has been on going now for, unbelievably over 3 years with a constant back and forth of attacks, but neither country wanting to escalate the situation. The war has been fought using primarily conventional weapons or military technology. There is good reason to believe that this just keeps going for the foreseeable future, as negotiations seem futile, and Russia does not seem like it is in any hurry to cease the fighting.

Middle East/Iran/Israel. The attack on Iran by the US caught many experts and investors off guard. After decades of threats and fears of a nuclear Iran, the reaction by the market was also surprising and 20 years ago, likely would have caused the market to correct. Instead, oil prices DROPPED, and the market rallied.

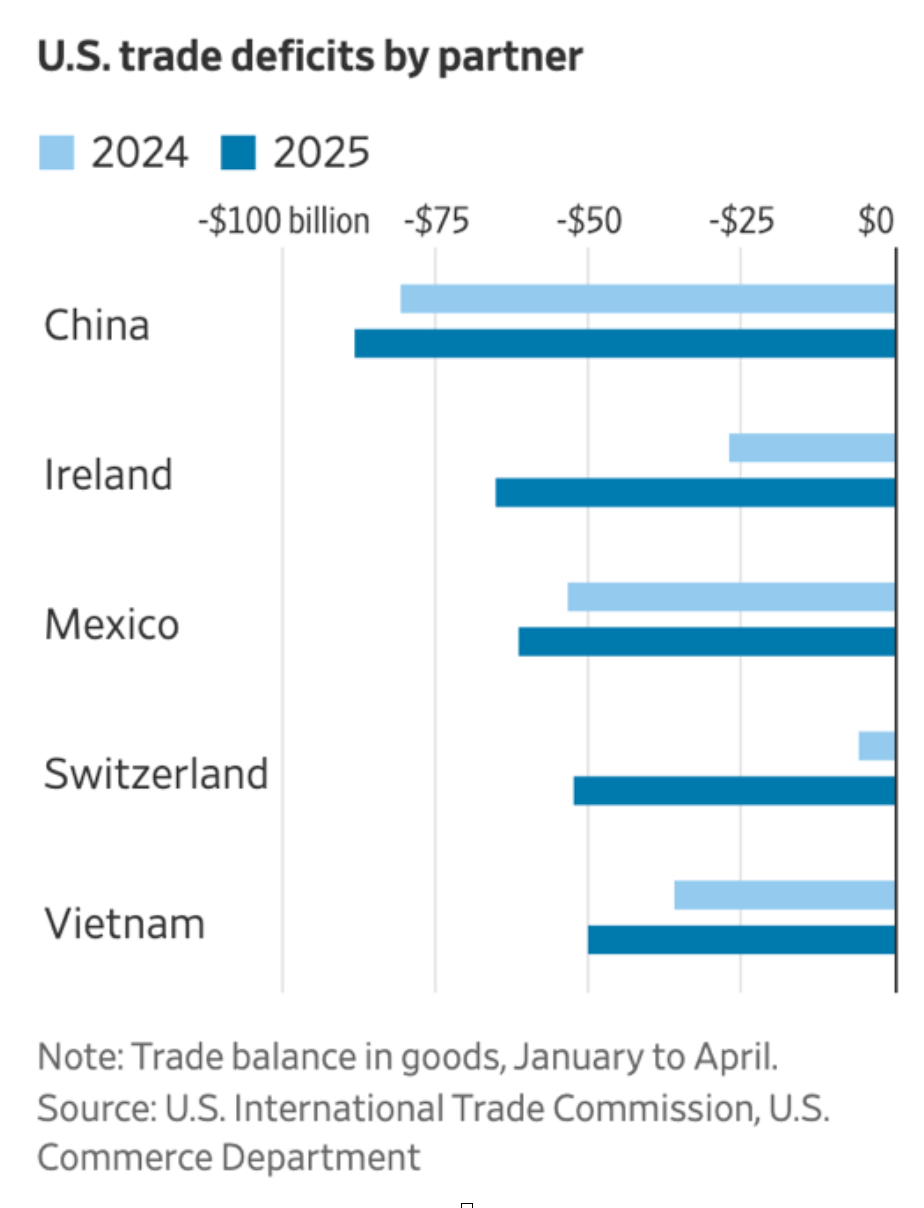

…from geopolitical events, we will segue into Tariffs once again. We wrote about how the Tariffs were calculated in our previous newsletter, and since then there has been a lot of back and forth with regards to raising and lowering them and pushing them out for 90 days so long as the country negotiated in good faith. We are right up at that 90 days and today’s news, and subsequent sell off was that Japan’s and South Korea’s would be “back” at the proposed 25% since no deal has been reached. Given the constant changes in this dynamic, stay tuned. The likely outcome, as with many countries, is that the minimal threshold will be set, and some type of deal will be reached.

Random sidebar…the country with the 2nd largest trade deficit in the first quarter of 2025 with the US is Ireland! The main driver for that is pharmaceuticals, led by GLP-1 treatments (diabetes and obesity drugs).

Aa1, AA+ and BBB (Big Beautiful Bill)

Moody’s downgraded the US government bonds to Aa1 from Aaa in mid-May. They were the last remaining agency that had the US that high. While no means early, as S&P cut to AA+ in 2011 and Fitch did the same in 2023, it does bring focus back to the increase in federal spending and tax cuts that are expected to increase the deficit (estimated by the CBO) by approximately $3.4T over the next 10 years.

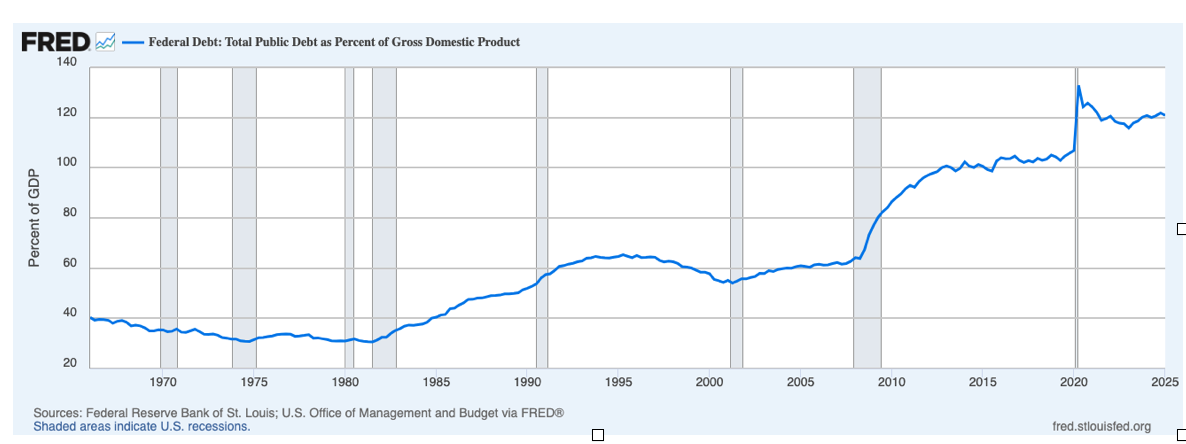

Government Debt Levels in the Last 25 Years…

- 2001-2007: Pre- 9/11 government debt was at $5.6T. This number increased to $9T right before the Global Financial Crisis (GFC) or The Great Recession. Debt to GDP went from 56% 62%. The primary driver for this was increased spending on homeland security, the Iraq war and tax cuts.

- 2008-2013: Government debt during this period went from $10T to $17T!!! Interestingly, household debt actually DECREASED from $13T to $11T. Increased spending for bailouts and lower tax revenue accounted for this dramatic increase. Wall St. vs Main St. was born.

- 2016-2019: When President Obama left office in 2017, debt levels were at $20T. In the subsequent 3 years, PRIOR to COVID, under President Trump’s first term, that number increased to $23T.

- 2020-2024: Multiple COVID Stimuli, a recession and rising interest rates drove debt levels up by unprecedented rates to $35T.

- 2025: We are now at $36T.

Debt to GDP

Not-so fun fact…

Prior to COVID, interest on our debt was $1b/day. It is currently over $2b/day. The reason for this is two-fold, the combination of higher debt (almost 50% higher) and higher interest rates (from nearly 0% to ~4-5%).

A few points from the Big, Beautiful Bill…

- Extends and makes permanent 2017 tax cuts with an increased standard deduction

- Increases deductions for seniors on Social Security

- Makes permanent write-offs for business interest expense and R&D

- Raises child tax credit slightly, raises state and local deductions for people earning <$500k and SALT cap reverts to $10k in 5 years from temporary increase to $40k in 2025

- Scaling back clean-energy incentives put in place by the Inflation Reduction Act (IRA)

- Starts Medicaid work requirements and drops the provider tax to 3.5% by 2028

- Raises the debt ceiling by $5T

- Requires states to cut the cost of SNAP benefits

Artificial Intelligence (AI) or Bust

Where to start? Per Sam Altman, the CEO of OpenAI, the evolution of AI capabilities is outlined in five stages:

- Chatbots: AI with conversational language skill, similar to basic ChatGPT interactions.

- Reasoners: AI that solves problems at a human level, working through complex issues and showing its reasoning. OpenAI’s o1 model.

- Agents: Systems that act autonomously and perform real-world tasks without constant human input.

- Innovators: AI that generates new scientific knowledge, creates breakthroughs, and develops novel solutions and discoveries.

- Organization: The most advanced stage, where AI systems can replicate and manage the complex functions of human organizations.

There has been much ado about “agentic AI” which puts us in Stage 3. As this plays out over the next several years, there will be significant dislocation and opportunity in the marketplace. This is something we will continue to closely monitor to gauge the impact to investment portfolios over the near and longer term.

AI, both directly and indirectly through ancillary innovations, in the last 18 months, has been viewed as the sole long term growth driver for the markets by many investors. We believe we are in the very early stages and believe this will continue to be an evolving opportunity for investors in the next decade. As AI evolves, so will the advances in other sectors like healthcare, “autonomous everything” and eventually robotics, which will aid significantly in the anecdote below…

Anecdote

We have written about demographics in previous newsletters now that Japan and China are in a population DECLINE situation and the potentially negative impact to their economies. We came across this chart and were alarmed that the majority of the developed world was at a fertility rate below 2.1 births per women which means that a population is not replacing itself naturally and hence eventually will be in population decline.

One of the worst situations is South Korea where in 2023 the rate is 0.72, down from 4.5 in 1970. What is potentially taking place there can be best described in this video link: South Korea Is Over . While many other factors come into play, all else being equal, after 2 generations (50 years) at this rate, the population will be ~13% of its current size.

Note: The US has a fertility rate of 1.6, which means in 2 generations we will be at 64% of our current size.

Conclusion

While it seems like there is a lot of chaos at the moment, the market has rallied back to all-time highs, though it continues to be concentrated in the mega-cap technology stocks. The weaker dollar and increased deficit spending has been positive for international markets for now, however we believe if the increased spending does not go beyond defense spending, the spread between US and international markets will narrow as the market will refocus on growth opportunities and the US markets provide a better opportunity for that.

The global unrest still seems isolated with minimal backlash from the wars for now, but we do continue to keep an eye on China and Taiwan as they may feel emboldened to push for an outcome more aggressively given the US’s actions globally.

US debt will remain an issue for years to come as not much has really been done to, at the minimum, try to narrow the deficit, but again, for now, there is not much pushback as we barrel towards $40T in debt. Having a potential tailwind of rate cuts in this situation is also helpful, as we know a big percentage of the interest we pay is driven by the higher rates of the last several years.

Finally, on a more positive note, as we are in the early innings of Artificial Intelligence (AI), there remains a long runway for growth and the new market opportunities it will create. As long as we have a cautious eye towards the social ramifications of what AI brings, it should be a net positive to financial markets and, more importantly, the world as it eventually bridges the social injustices and economic inequities that exist today.

DISCLOSURES

The information contained herein reflects the opinion and projections of Bergamot Asset Management LP (“Bergamot”) as of the date of publication, which are subject to change without notice at any time subsequent to the date of issue. Bergamot does not represent that any opinion or projection will be realized. All information provided is for informational purposes only and should not be deemed as investment advice or a recommendation to purchase or sell any specific security. This shall not constitute an offer to sell or the solicitation of an offer to buy any interest in any fund managed by Bergamot or any of its affiliates. While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any data presented. This communication is confidential and may not be reproduced without prior written permission from Bergamot. Market conditions can vary widely over time and can result in a loss of portfolio value. Past performance does not guarantee future results.