Spring Update – April Showers Bring May Flowers…

“The strongest of all warriors are these two – Time and Patience.”

War and Peace – Leo Tolstoy

Happy Spring to all. After a pretty brutal winter in the northeast relative to the past several years and a challenging market backdrop after three strong years in the market we are viewing the pullback as healthy and with “time and patience,” long term investors will be rewarded.

Quick summary:

A look at the various indices in 2025, before the attack on Iran (2/27/26) and after the attacks through this past Friday (3/27/26):

| 12/31/2024 | 12/31/2025 | 2/27/2026 | 3/27/2026 | |

|---|---|---|---|---|

| S&P 500 | 5881.63 | 6845.50 | 6878.88 | 6368.85 |

| DJIA | 42544.22 | 48063.29 | 48977.92 | 45166.64 |

| Nasdaq | 19310.79 | 23249.99 | 22668.21 | 20948.36 |

After a strong 2025 where the S&P 500 was up 16%+ and the Nasdaq 20%+, both indices got off to non-eventful starts where new highs were set but were quickly followed by drawdowns. With the onset of the war in Iran – Operation Epic Fury and the subsequent rise of oil prices, the market in the last week has sold off fairly significantly and has entered “correction” territory (a short-term drop of 10% or more from its recent peak).

What is on our mind? War. The Economy. Inflation. Unemployment. Interest Rates.

While that seems like a lot, many of the concerns for the market are interconnected. Starting with Iran and Operation Epic Fury. On February 28, 2026, the US and Israeli military began attacks on Iran. The obvious reaction to markets was a sharp increase in the price of oil where it went from roughly $60 before the attacks, to roughly $100. This is unfortunate timing as we start to head into peak driving season, as prices at the pump have increased by over $1/gallon, putting further pressure on what is already a challenged consumer, especially those at the lower-income level. Interestingly enough, September futures for oil are priced at $75, so while it does not appear that there is an end in sight in the near term, the market is expecting that this will be mostly “over” by fall.

Unemployment

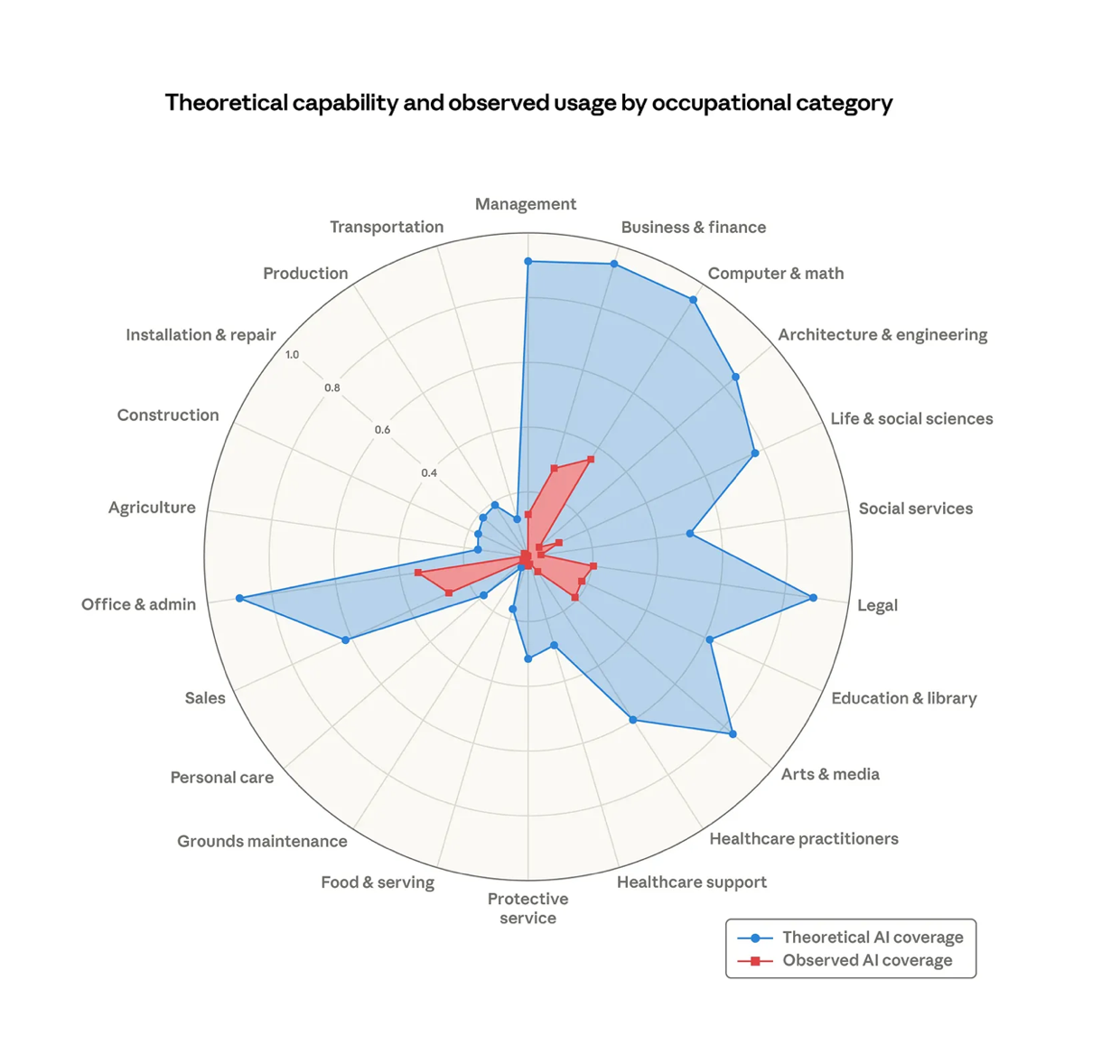

On unemployment, U.S. companies had the largest number of January job cuts since 2009, but almost 50% of cuts are tied to Amazon (AMZN) 16k, UPS (UPS) 30k, and Dow (DOW) 4500 reports Bloomberg. Other honorable mentions are Nike (NKE) and Peloton (PTON). While companies have the tendency to “blame AI” for the job cuts, we believe at this time, that many of the announced cuts are more of an “excuse” to compensate for some of the over hiring that took place during and slightly after COVID. What is concerning, is that inevitably, we do believe that job cuts from AI will be impactful. Anthropic’s CEO recently warned that “AI-driven white-collar jobs bust” is a significant risk and suggest that up to 50% of entry-level white-collar roles could be automated within five years. We are already seeing the challenges college graduates are facing in finding new jobs. If even a fraction of that 50% occurs, there will be significant implications.

Below is a visual of what was discussed by Anthropic:

The Economy. Financials. Private Credit.

Usually, as financials go (ie bad debt, over leveraging, etc.), so goes the market as debt and lending is “what makes world go ‘round.” Private Credit has been a big growth driver in recent years. It is estimated that the global market has expanded from roughly $375 billion in 2013 to over $2.5 trillion in recent years. What was once considered “shadow banking” has not been as closely monitored by agencies as deals are generally not transacted on the public market but is now a big part of global lending.

Recently, there has been some concern on some smaller companies like Blue Owl and Stone Ridge seeing issues. This has caused “redemption gating” by BlackRock, Apollo, and Morgan Stanley in Q1 2026 and confirms some of the stress: perceived stress initiates redemption pressure, which creates actual stress through forced asset liquidation. There are significant maturities in 2028 to 2031 that potentially compounds refinancing risk. While all the larger companies say that the risk in losses is small and isolated, it is something that bears monitoring.

Real Estate, a category we do not often speak about given the strength in the past decade has seen some mixed data. Some datapoints:

- J.P. Morgan moves to offload large CRE loan exposure, including office exposure as part of an effort to reduce balance sheet risk. It is not coincidental that Jamie Dimon has been a big proponent of returning to the office.

- Carlyle targeting distressed US Real Estate Equity.

- Office-to-Residential conversions face reality check due to constraints in cost, design limitations and feasibility challenges.

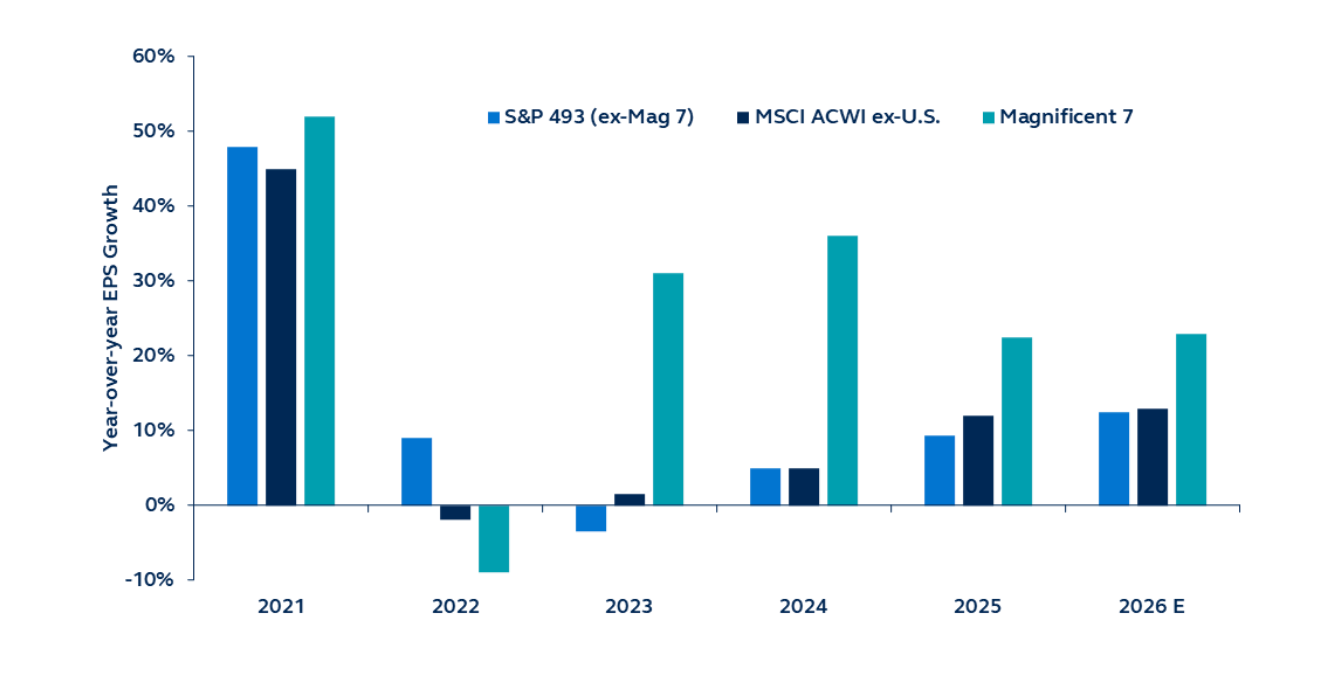

Artificial Intelligence (AI) and the Magnificent 7.

AI is the sector that is most scrutinized due to importance in growth for the markets and also the relative sizing in the Magnificent 7 and hence the outsized weight in the major indices. As can be seen below, these companies have made up a big percentage of year-over-year growth and will continue to be so…

One of the interesting things is the amount being spent on AI infrastructure (capex, including NVIDIA chips). The plans for 2026 from some these companies are: Amazon (AMZN) $200b ($45b in stores), Alphabet (GOOGL) $175-185b, Meta (META) $115-135b, Microsoft (MSFT) $145-150b. That is almost $1 trillion and up year-over-year!!! This will be another area to monitor, as the growth in capex spend should moderate in coming years.

Conclusion

While there has been a lot of volatility to start the year, it is healthy to have a little bit of a selloff after 3 strong years in the market. Note, 2025 also started with some volatility because of the tariffs. Oil prices, while currently high, will drop when the war ends, and its contribution to higher inflation (which is reported ex- food and energy) will truly be (I will dare use the word) “transitory.”

Earnings estimates for the S&P 500 for 2026 are roughly $305-310, and north of $350 for 2027. All else being equal, the market is not expensive given the projected growth. Interest rate cuts will still be a tailwind for the market once we get through this oil shock/inflation concern and generally should provide support for the market overall. “Time and patience” will ultimately prevail as the market refocuses on fundamentals and growth.

The information contained herein reflects the opinion and projections of Bergamot Asset Management LP (“Bergamot”) as of the date of publication, which are subject to change without notice at any time subsequent to the date of issue. Bergamot does not represent that any opinion or projection will be realized. All information provided is for informational purposes only and should not be deemed as investment advice or a recommendation to purchase or sell any specific security. This shall not constitute an offer to sell or the solicitation of an offer to buy any interest in any fund managed by Bergamot or any of its affiliates. While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any data presented. This communication is confidential and may not be reproduced without prior written permission from Bergamot. Market conditions can vary widely over time and can result in a loss of portfolio value. Past performance does not guarantee future results.