Fall/Winter Update

"Winter is the time for comfort, for good food and warmth, for the touch of a friendly hand and for a talk beside the fire: it is the time for home." – Edith Sitwell

Happy Thanksgiving to all! We hope you had a nice holiday and were able to spend time with family and friends. As we pass the midway point of the final quarter for 2025, we would like to review what has happened so far this year and, more importantly, what we are focusing on for 2026.

Briefly, the 3rd quarter was solid once again with returns as follows:

- The S&P 500 gained 7.79%.

- The Nasdaq 100 surged 8.82%.

- The Dow Jones Industrial Average rose 5.22%.

The year is solidly in the black for the third year in a row, despite the market concerns earlier this year that included: Deepseek, tariffs, trade wars, government shutdown and global unrest in Ukraine and the Middle East.

Government Shutdown…to be continued. The government shutdown has been temporarily resolved (thankfully before the holidays). The bill passed by Congress and signed by the President funds the government until January 30 with carveouts for SNAP, benefits targeted at women, infants and children, or WIC, the Department of Veterans Affairs and Congress. Those will all be funded through the end of September 2026.

What financial impacts could Americans experience?

- Essential financial benefits will continue: The good news is that many core federal services remain operational. Social Security, Medicare, and Medicaid benefits will continue to be distributed. Veterans’ benefits will also remain in place. The Supplemental Nutrition Assistance Program (SNAP) and the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC) will continue as funds allow. Most IRS operations, including tax filings and refunds, are expected to proceed as well.

- Delays are likely in some government services: Depending on the duration of the shutdown, the delivery of some government services may be delayed. These can include federal housing loan approvals through the Federal Housing Administration (FHA), the Department of Housing and Urban Development (HUD), and the United States Department of Agriculture (USDA). The processing and approving of new SBA 7(a) and CDC/504 loans are paused. Key federal data reports — such as those related to employment or inflation — could be postponed.

- Federal employees may be affected: Many federal employees are currently furloughed or working without pay. While backpay is typically issued once funding is restored, the uncertainty and disruption can be difficult for those impacted.

- Broader economic impact is possible: Short-term government shutdowns have historically had a limited impact on financial markets. However, a prolonged disruption can affect consumer confidence, delay economic data reports, and impact federally supported programs. Depending on shutdown length, this could be especially significant for the Federal Reserve, which meets at the end of October and relies on jobs and inflation reports to guide decisions on interest rates.

While the impacts are pretty widespread, as we experienced, and there is a risk that we re-shutdown in February, the impact for the markets should be short-term in nature, as we saw for what was the longest shutdown in recent years.

What are we thinking about?

Interest Rates. This is a topic we cannot seem to stop mentioning in our newsletters despite every effort to, as it remains one of the keys to providing a “floor” to the market. The current Fed funds rate is targeted at 3.75% - 4.00% down from 5.25% - 5.50% in 2023. With another reduction expected in December, and some analysts targeting it to be below 3.00% by the end of 2026, this will continue to be a tailwind for the market. We hope it leads to broader market strength as the lower rates should disproportionately help capital intensive industries and more broadly the consumer due to lower rates for mortgages, automobiles and other high-ticket items.

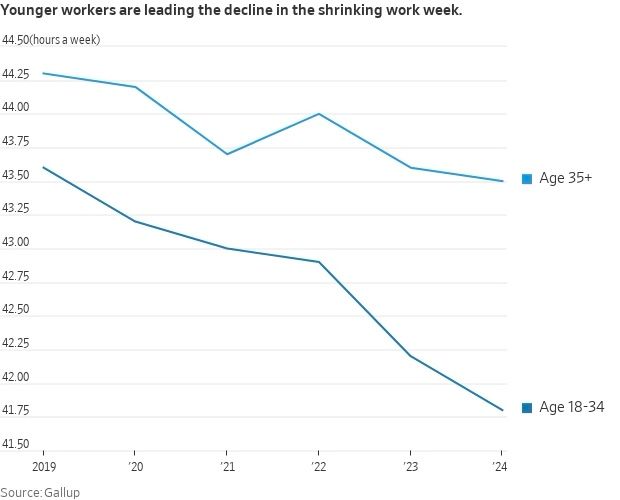

Unemployment. Weak employment is one of the key factors that is allowing the Fed to lower interest rates, despite some ongoing fears of inflation. The labor market is showing significant weakness for younger workers, especially recent college graduates.

Another point of weakness is layoffs that are being attributed to AI directly or indirectly, from companies. Some of these include Amazon (14k), Accenture (11k), Intel (21k), and Microsoft (15k). Other layoffs are more general (restructuring/cost-cutting) in nature, such as UPS (46k) and Verizon (13k). What is concerning about the bulk of these layoffs is that a large percentage of them are high paying, white-collar jobs.

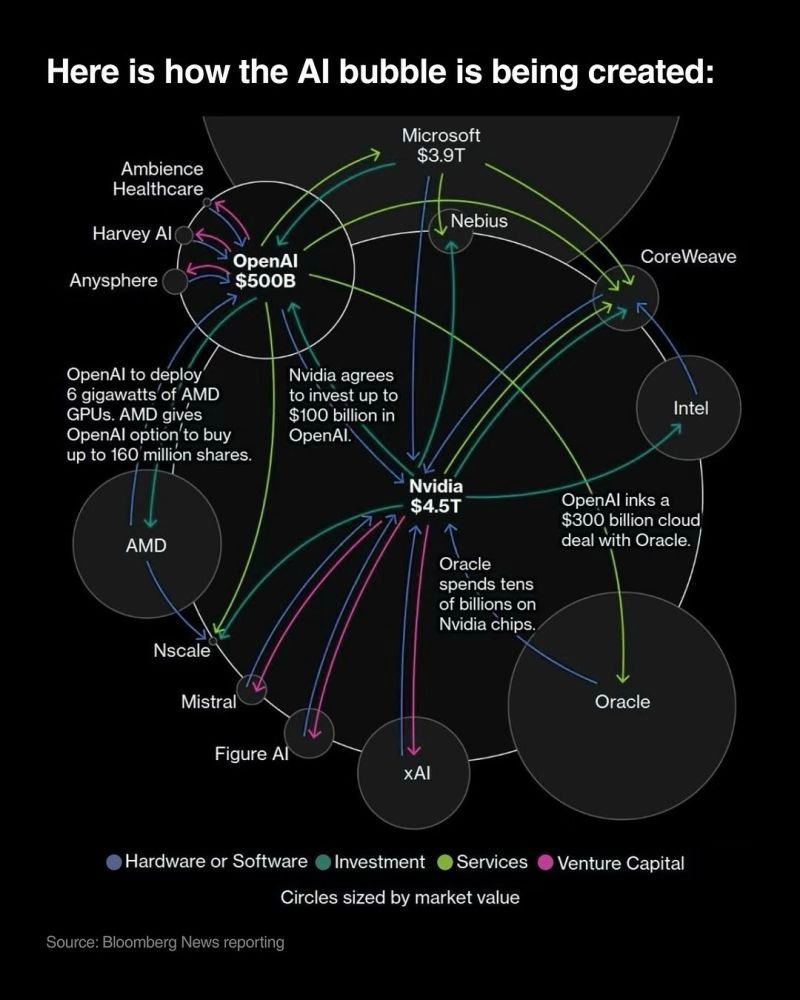

Artificial Intelligence (AI). The same way the internet was one of the biggest technological innovations or advances in the past 30 years, Artificial Intelligence (AI) is going to be the biggest technological advancement in the years to come. Hundreds of billions, if not trillions, of dollars are being committed and invested to build the supporting infrastructure and similar to the early 2000s, there is now a lot of conversation about “bubbles.” This chart from Bloomberg about a month ago illustrated best why the concerns are increasing.

Since this was published, there have since been hundreds of billions of additional announcements similar to the one illustrated above.

Anecdotes.

- Black Friday sales climbed 4.1%, Mastercard said, surpassing last year’s growth, a sign US consumers are continuing to spend despite persistent economic concerns. But Adobe Analytics expects growth in Cyber Monday sales to ease from last year. - Bloomberg

- For years it has seemed no sticker price was too high for American car buyers. Even as average new car prices approached $50,000 this year, dealers fretted more over depleted inventories than losing customers to sticker shock. Those days may be ending as increasingly stretched consumers are starting to draw the line on what they will pay for a new car, according to dealers, analysts and industry data. - Wall Street Journal

- The bond market is straining to absorb a flood of new bonds from tech companies funding their artificial intelligence investments, adding to the recent pressure in markets. Since the start of September, so-called AI hyperscalers Amazon, Google, Meta, and Oracle have issued nearly $90 billion of investment-grade bonds, according to Dealogic, more than they had sold over the previous 40 months. - Wall Street Journal

- AI music generator Suno closed a $250 million Series C round at a $2.45 billion post-money valuation. The company is expected to generate $200 million in annual revenue. - Music Business Worldwide

Conclusion

As has been consistent for most of the past couple years, there has been a lot of noise in the news that has had moderate short-term negative impact to the markets, however, the strength of investments in Artificial Intelligence has been overwhelmingly positive and driven the market to all-time highs. While we are long term believers in technology, and the value it generally brings to global economies, we are currently more balanced as companies have been spending tremendous amounts of money to build the underlying infrastructure and we wait for the increase in practical use cases of the technology to be more widely adopted.

With estimates for earnings of the S&P 500 targeted to be $305.00 in 2026 and $344.00 in 2027 and additional interest rates expected in 2026, the market is not unreasonably expensive at ~20x 2027 earnings expectations given the 13% targeted growth rate. That being said, it will be important to watch the adoption ramp of AI applications and the broadening impact of lower interest rates to the companies beyond the Magnificent 7 (ie the remaining 493 companies in the S&P 500).

The information contained herein reflects the opinion and projections of Bergamot Asset Management LP (“Bergamot”) as of the date of publication, which are subject to change without notice at any time subsequent to the date of issue. Bergamot does not represent that any opinion or projection will be realized. All information provided is for informational purposes only and should not be deemed as investment advice or a recommendation to purchase or sell any specific security. This shall not constitute an offer to sell or the solicitation of an offer to buy any interest in any fund managed by Bergamot or any of its affiliates. While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any data presented. This communication is confidential and may not be reproduced without prior written permission from Bergamot. Market conditions can vary widely over time and can result in a loss of portfolio value. Past performance does not guarantee future results.